The Hidden Costs of Debt: It’s Draining Your Wealth and Well-Being

Introduction

Debt is often seen as a necessary part of life. Whether it’s student loans, mortgages, car payments, or credit card balances, borrowing money can sometimes feel unavoidable. However, what many people fail to realize are the hidden costs of debt—the expenses and consequences that go far beyond the monthly payment.

These hidden costs can impact everything from your stress levels to your financial future. In this article, we’ll uncover these hidden expenses, explain how they affect you in ways you might not expect, and provide strategies to minimize their impact.

Understanding the Hidden Cost of Debt

Most people think of debt in terms of interest rates and minimum payments. But debt comes with additional financial and emotional costs that can drain your resources over time. Let’s explore some of the most damaging hidden costs of debt and why they matter.

1. The Hidden Cost of Debt and Its Psychological Toll

One of the most overlooked hidden costs of debt is the psychological burden it creates. Research has shown that high levels of debt are linked to increased stress, anxiety, and even depression.

- Constant worry about payments can lead to sleepless nights.

- Debt stress can strain relationships and family life.

- The feeling of being financially trapped can contribute to poor mental health.

Over time, this mental burden can also lead to decreased productivity at work, strained friendships, and even feelings of hopelessness. Many people don’t realize how deeply debt affects their daily mood and ability to focus on personal and professional growth. Debt stress and mental health are closely linked, making it critical to address these hidden costs early.

2. The Long-Term Interest Trap of Debt

Interest is the most obvious cost of borrowing, but its long-term effects are often underestimated. Even a low-interest loan can cost thousands over its lifetime.

For example, let’s say you have a $10,000 credit card balance with a 20% interest rate and only make minimum payments. You could end up paying double or even triple the original amount over time!

The real danger? Many people don’t realize how much money they’re throwing away on interest instead of using it for savings, investments, or emergency funds. Even small changes in payment strategy—such as paying slightly more than the minimum each month—can drastically reduce how much you pay in interest over time.

3. Opportunity Cost: How the Hidden Cost of Debt Steals from Your Future

Every dollar you spend on debt repayment is a dollar you can’t use elsewhere. This concept, known as opportunity cost, is one of the biggest hidden costs of debt.

- Money spent on high-interest debt could have been invested for retirement.

- Paying off loans instead of saving means missing out on compound interest benefits.

- Debt repayment can delay major financial goals like buying a home or starting a business.

Think of debt as a silent thief—it’s not just taking money from you today, but also robbing you of potential wealth in the future. Those who aggressively pay down debt earlier in life often find themselves in much better financial positions later on.

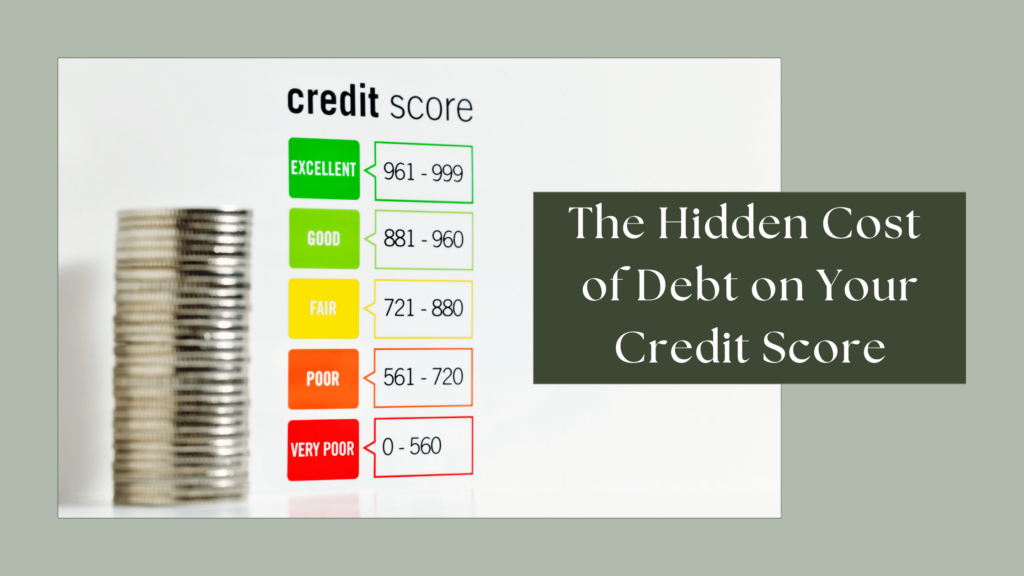

4. The Hidden Cost of Debt on Your Credit Score

A high debt balance can negatively impact your credit score, which affects your ability to borrow money in the future. A lower credit score can lead to:

- Higher interest rates on future loans.

- Difficulty securing a mortgage or car loan.

- Higher insurance premiums.

- Limited rental opportunities (many landlords check credit scores).

Many people don’t realize just how much a poor credit score can cost them over time. For example, a higher interest rate on a mortgage due to a low credit score could mean paying tens of thousands more over the life of the loan. Learn how to improve your credit score to avoid these hidden costs.

5. Increased Insurance Costs Due to Debt

Surprisingly, your credit score can affect your insurance rates. Many insurance companies use credit-based insurance scores to determine premiums. Poor credit can mean paying significantly more for auto, home, and even life insurance.

A lower credit score can signal financial instability, which some insurers interpret as an increased risk of missed payments. Even if you have a clean driving record, you could still be paying higher premiums simply because of your credit rating. Over time, these increased costs can add up to thousands of dollars, making it even harder to get out of debt. Understanding credit-based insurance scores can help you navigate this hidden cost.

6. The Hidden Cost of Debt on Career Opportunities

Some employers check credit reports as part of the hiring process, especially for jobs that involve handling money or sensitive information. If your credit report is filled with late payments or high debt, it could hurt your chances of landing a job.

Certain career paths, such as finance, law enforcement, and government positions, often require a strong financial track record. Even if a job doesn’t explicitly require a credit check, struggling with debt-related stress can negatively impact work performance and career progression.

7. How the Hidden Cost of Debt Strains Relationships

Debt isn’t just a personal issue—it affects relationships, marriages, and family dynamics. Financial stress is one of the leading causes of relationship problems and divorce. When one or both partners are overwhelmed by debt, it can lead to:

- Frequent arguments about money.

- Resentment over spending habits.

- Difficulty planning a future together.

Debt can also influence major life decisions such as marriage, having children, or buying a home. The burden of debt can delay or even derail these important milestones.

8. Health Problems Linked to Debt Stress

Financial stress doesn’t just affect your mind—it impacts your physical health, too. Studies have found that people in high debt situations are more likely to experience:

- High blood pressure.

- Increased risk of heart disease.

- Chronic headaches and migraines.

- Poor diet and lack of exercise due to financial constraints.

9. The Generational Impact of the Hidden Cost of Debt

Debt doesn’t just affect you—it can impact your children and future generations. Parents struggling with debt often find it harder to save for their children’s education, making it more likely that their kids will also have to rely on loans. This cycle of debt can repeat itself for generations.

Additionally, when parents are burdened by debt, they may have fewer financial resources to pass down to their children, leading to limited financial literacy and fewer opportunities for wealth-building. Many young adults start their financial journeys already saddled with student loans and credit card debt, making it difficult to achieve milestones such as homeownership or retirement savings. Breaking the cycle of generational debt requires education, financial planning, and proactive debt management.

10. The Risk of Never Truly Being Debt-Free

For some, debt becomes a way of life. They move from one loan to the next, never fully escaping the cycle. This continuous borrowing prevents financial freedom and keeps people trapped in a paycheck-to-paycheck existence.

Many people assume they will always have some form of debt, but breaking free is possible with careful planning and disciplined financial habits.

Conclusion: Break Free from the Hidden Cost of Debt

Debt isn’t just about numbers—it affects every aspect of your life. From emotional stress to lost opportunities, the hidden cost of debt is far greater than most people realize. However, taking proactive steps today can lead to a more financially secure and stress-free future.

At Debt Medic, we’re here to help you take control of your financial future. Whether you need debt relief options or financial guidance, we’re ready to support you every step of the way.

Are you ready to break free from the hidden cost of debt? Contact Debt Medic today and start your journey to financial freedom!