Financial MythBusters – The Truth About Tax Brackets

Myth #1 – “It’s not worth it to move into a

higher tax bracket as I will make less money!”

Welcome to one of our Financial MythBusters blogs. This is David Senft here at Debt Medic and I wanted to do this particular topic today, as I do here from time to time with different clients and individuals that I have now. As I was growing up hearing people saying things like, “it’s not worth it to move into the next higher tax bracket because many times you lose too much money or you’re going to get taxed more. You’ll probably even make less money.” So I’d like to explain to you today how the tax brackets work, how you get taxed, and to show you what you can expect. And should you take that next raise, will it put less money in your pocket or will it put more money into your pocket?

So let’s take a look and I’m going to do this by first, starting with the federal income tax brackets. Now, I do want to mention that every province also has different marginal tax rates or tax brackets. So I’m not going to be putting those onto the slides that you’re going to see, but I will put links to them at the end of the blog so that you can click and go see what the tax rates are in your province because you’ll have both the federal and provincial tax rates combined for the taxes that you will be paying – whether you like it or not. Right?

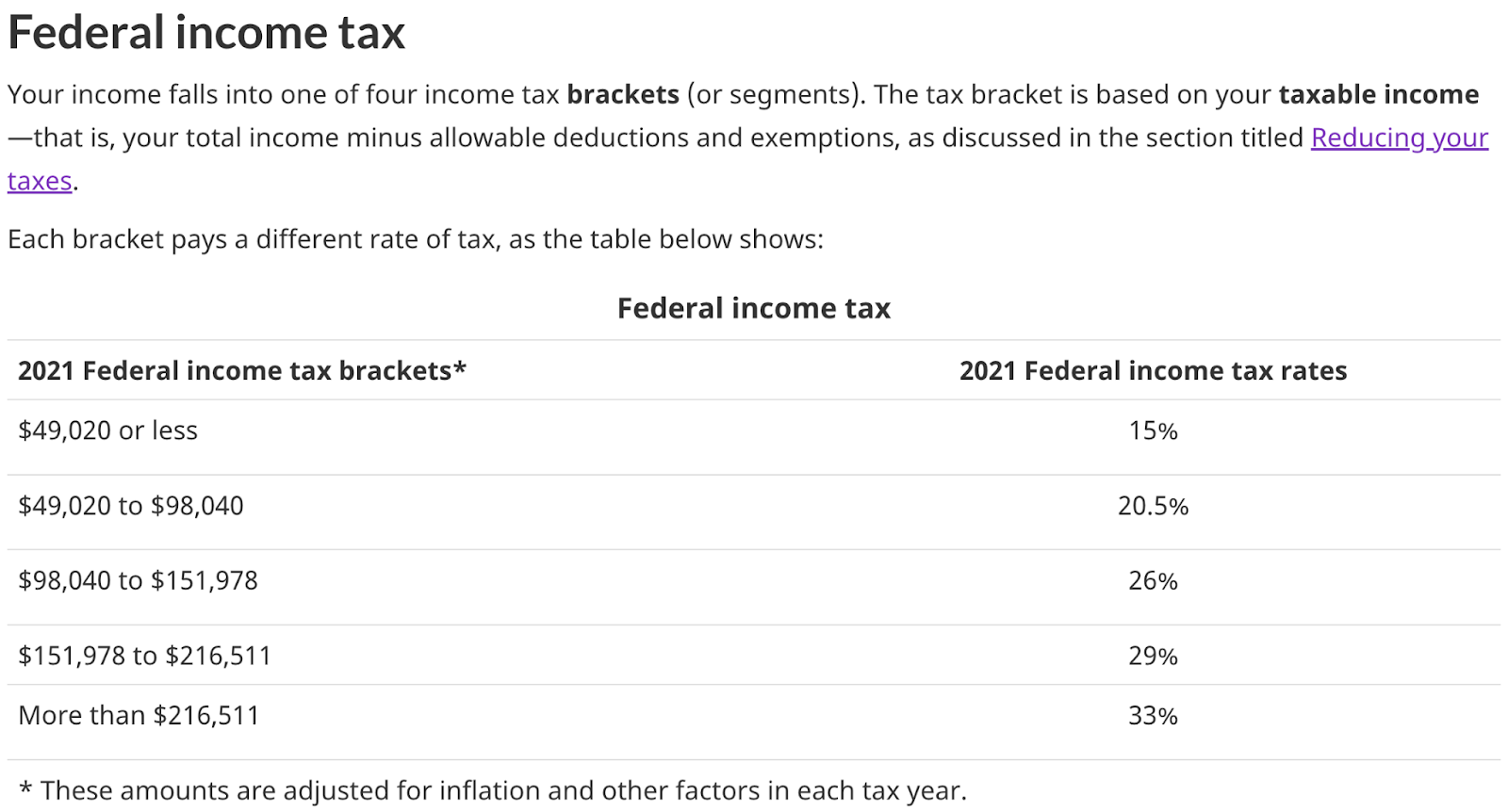

So just a quick little look here at that first sentence. Your income falls into one of four tax brackets, and the tax bracket is based on your taxable income. So when you’re paying taxes, you’re not paying taxes on every dollar that you earn. There are some things that you can deduct from your income in order to end up with a taxable income. That is the amount that you’re taxed on, and that’s the amount that depends on the tax bracket that you’re in. In 2021 the federal income tax rates varied, starting at 15% on your taxable income. Your federal income tax brackets started at $49,020 or less. So if that was the amount of money that was your net income, your taxable income, you would be paying 15% of that amount to the government. Now, if you make over $49,020 and all the way up to basically double that $98,040, your income tax rate goes to 20.5%.

Now, the important thing, and what most people misunderstand is that they think if they earn more than $49,000, they’re going to get charged 20.5% tax on all of the money that they earn. But actually, you’re only paying the 20.5% on the amount above $49,020. And so it does not affect the 15% you paid on the amount below that, okay? Now, if you make more than $98,040, every dollar you earn above $98,040, you’ll be paying 26% all the way up until your income hits $151,000, et cetera. So this is something that a lot of people don’t understand, is that it’s broken up into these different components in terms of the amount of tax you pay on this.

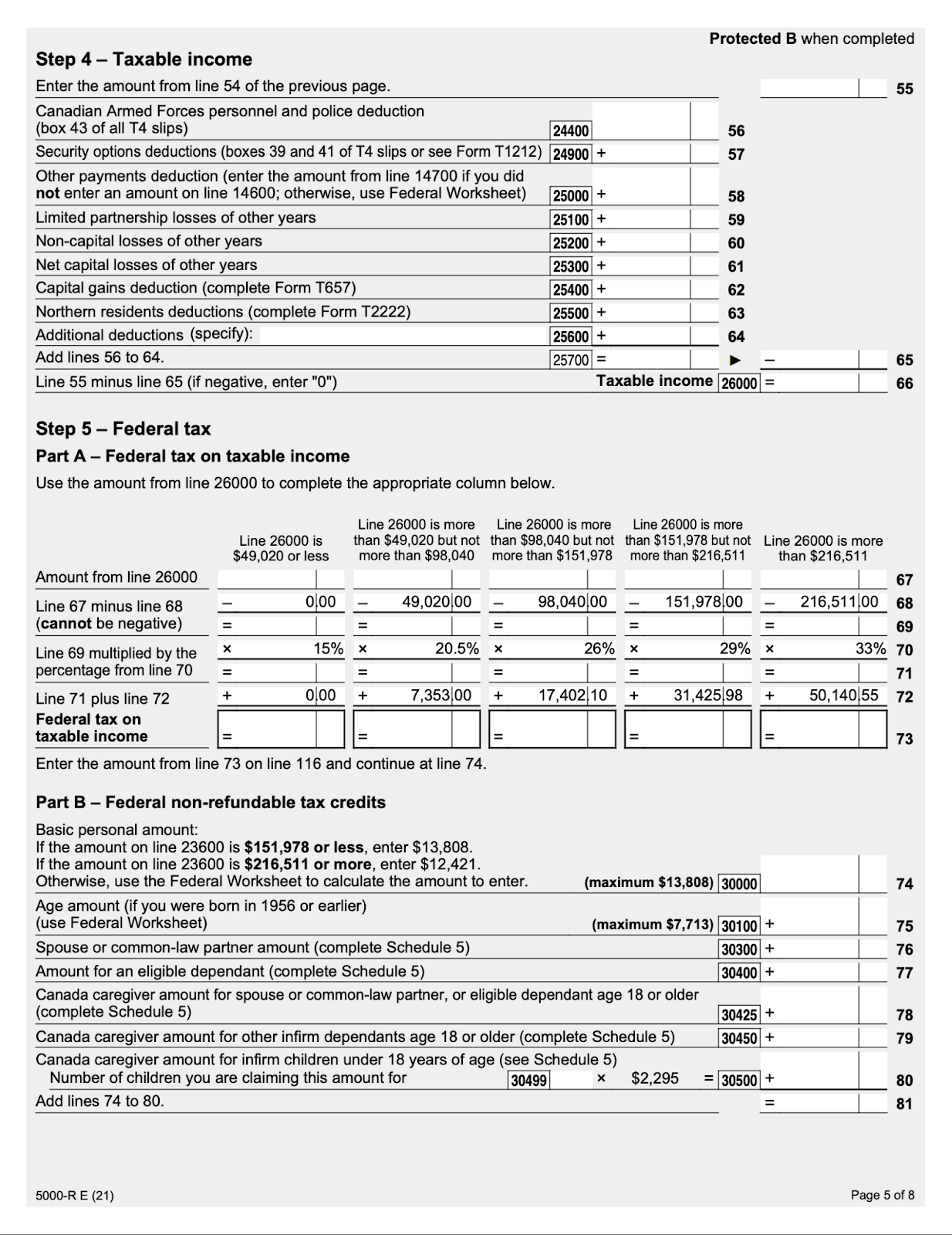

So the way it looks on your tax form, I just want to pull up these tax forms here, the first couple of pages of your income tax form. They’re just asking for all your personal information.

And then on the third page of your tax form, you put your total income on that page. So that’s going to be all the income from your T-four slips, any other kinds of income that you have, CPP, old age security, withdrawing RSPs – all of that goes here on the first page that gives you your total income.

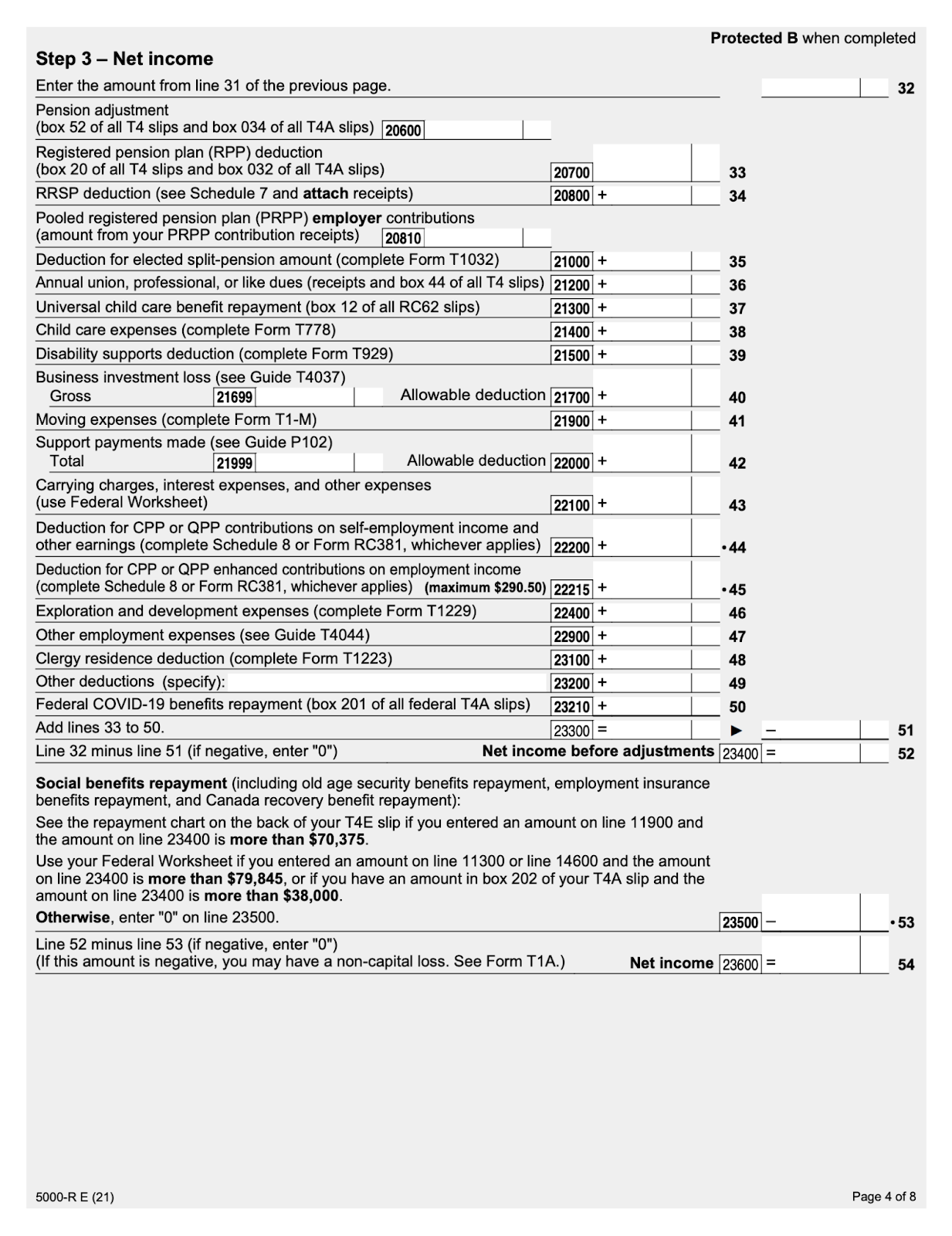

Then on the next page of your tax return, you’re going to calculate your net income. There are some different options of things that they will allow you to deduct from your total income. And so you won’t be paying tax on those portions. So you can see, looking at this, things like your RRSP contributions that you make, different pension amounts that you contribute through your employment, and your deductions for your CPP and your EI, all of these things come off of your gross income. And it allows you to calculate a net income here at the bottom of this page.

Now, we’re not done yet. There still are some additional items that you can deduct off of this, and that would be on the next page of your tax form.

It’s now going to calculate your taxable income. So there are a few additional unique things, like if you have northern residence deductions and some other things, you can do some further deductions off your income to come to this line on your tax return called taxable income. Once you have that determined, they then have a table on your tax form that allows you to put in the amount that you owe. And you can see that the tax brackets are laid out here on this form that is showing you up to your 1st $49,020. You’re going to pay 15%, then it increases to 20.5%, et cetera. As your income increases in the new bracket, they’re only going to charge you that rate on the amount that you earn in that next tax bracket.

So here’s a really great example. If your taxable income was $50,000 – so you’ve just entered into that second tax bracket. Now, if your entire income was going to be taxed at 20.5%, you’d be paying well over $10,000 in taxes. But that’s again, not how it works. So here’s how it would calculate. You’d pay 15% on the first amount, up to $49,020, which is $7,353, and then you’d pay 20.5% on the amount over $49,000. So that’s only around $1,000. So in this example, you’d pay $200.90 in taxes on that portion, giving you a total federal tax of $7,553. So it’s not $10,000. You’re not paying that 20.5% of the whole amount just on that last thousand dollars that you earned.

So I hope that sort of clears it up for you. If you’re ever offered that raise at work, a new position where you’re offered more money, don’t be scared that, “Oh no, I’m going to be in a new tax bracket, the only raise I’m getting is in responsibilities – I’m not going to make any more money.” That’s not true. You will pay a little bit higher tax on those higher dollars, but it’s still, at the end of the day, putting more money in your pocket that you can use to live and increase your quality of life. So hopefully that helps clear that up for some of you and have an awesome day!

The following information comes from the Canadian Government website: https://www.canada.ca/en/financial-consumer-agency/services/financial-toolkit/taxes-quebec/taxes-quebec-2/6.html

Income tax rates in Quebec are higher than in other provinces and territories because the government of Quebec finances a wide variety of services that other governments do not. You can use the chart below to see the tax brackets and rates for other provinces and territories.

| Provinces / Territories | Rates for 2021 tax year |

|---|---|

| Newfoundland and Labrador | 8.7% on the first $38,081 of taxable income, + 14.5% on the next $38,080, + 15.8% on the next $59,812, + 17.3% on the next $54,390, + 18.3% on the amount over $190,363 |

| Prince Edward Island | 9.8% on the first $31,984 of taxable income, + 13.8% on the next $31,985, + 16.7% on the amount over $63,969 |

| Nova Scotia | 8.79% on the first $29,590 of taxable income, + 14.95% on the next $29,590, + 16.67% on the next $33,820, + 17.5% on the next $57,000, + 21% on the amount over $150,000 |

| New Brunswick | 9.68% on the first $43,835 of taxable income, + 14.82% on the next $43,836, + 16.52% on the next $54,863, + 17.84% on the next $19,849, + 20.3% on the amount over $162,383 |

| Quebec | 15% on the first $45,105 of taxable income, + 20% on the next $45,095, + 24% on the next $19,555, + 25.75% on the amount over $109,755 |

| Ontario | 5.05% on the first $45,142 of taxable income, + 9.15% on the next $45,145, + 11.16% on the next $59,713, + 12.16% on the next $70,000, + 13.16% on the amount over $220,000 |

| Manitoba | 10.8% on the first $33,723 of taxable income, + 12.75% on the next $39,162, + 17.4% on the amount over $72,885 |

| Saskatchewan | 10.5% on the first $45,677 of taxable income, + 12.5% on the next $84,829, + 14.5% on the amount over $130,506 |

| Alberta | 10% on the first $131,220 of taxable income, + 12% on the next $26,244, + 13% on the next $52,488, + 14% on the next $104,976, + 15% on the amount over $314,928 |

| British Columbia | 5.06% on the first $42,184 of taxable income, + 7.7% on the next $42,185, + 10.5% on the next $12,497, + 12.29% on the next $20,757, + 14.7% on the next $41,860, + 16.8% on the next $62,937, + 20.5% on the amount over $222,420 |

| Yukon | 6.4% on the first $49,020 of taxable income, + 9% on the next $49,020, + 10.9% on the next $53,938, + 12.8% on the next $348,022, + 15% on the amount over $500,000 |

| Northwest Territories | 5.9% on the first $44,396 of taxable income, + 8.6% on the next $44,400, + 12.2% on the next $55,566, + 14.05% on the amount over $144,362 |

| Nunavut | 4% on the first $46,740 of taxable income, + 7% on the next $46,740, + 9% on the next $58,498, + 11.5% on the amount over $151,978 |